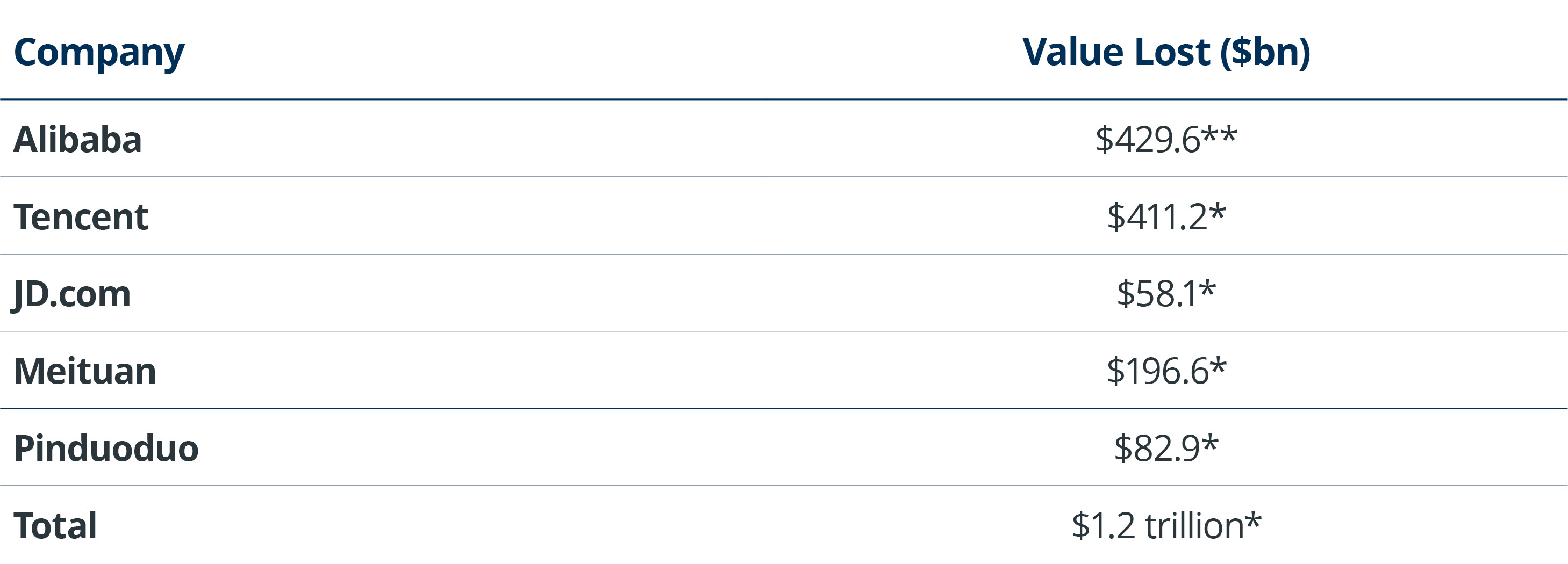

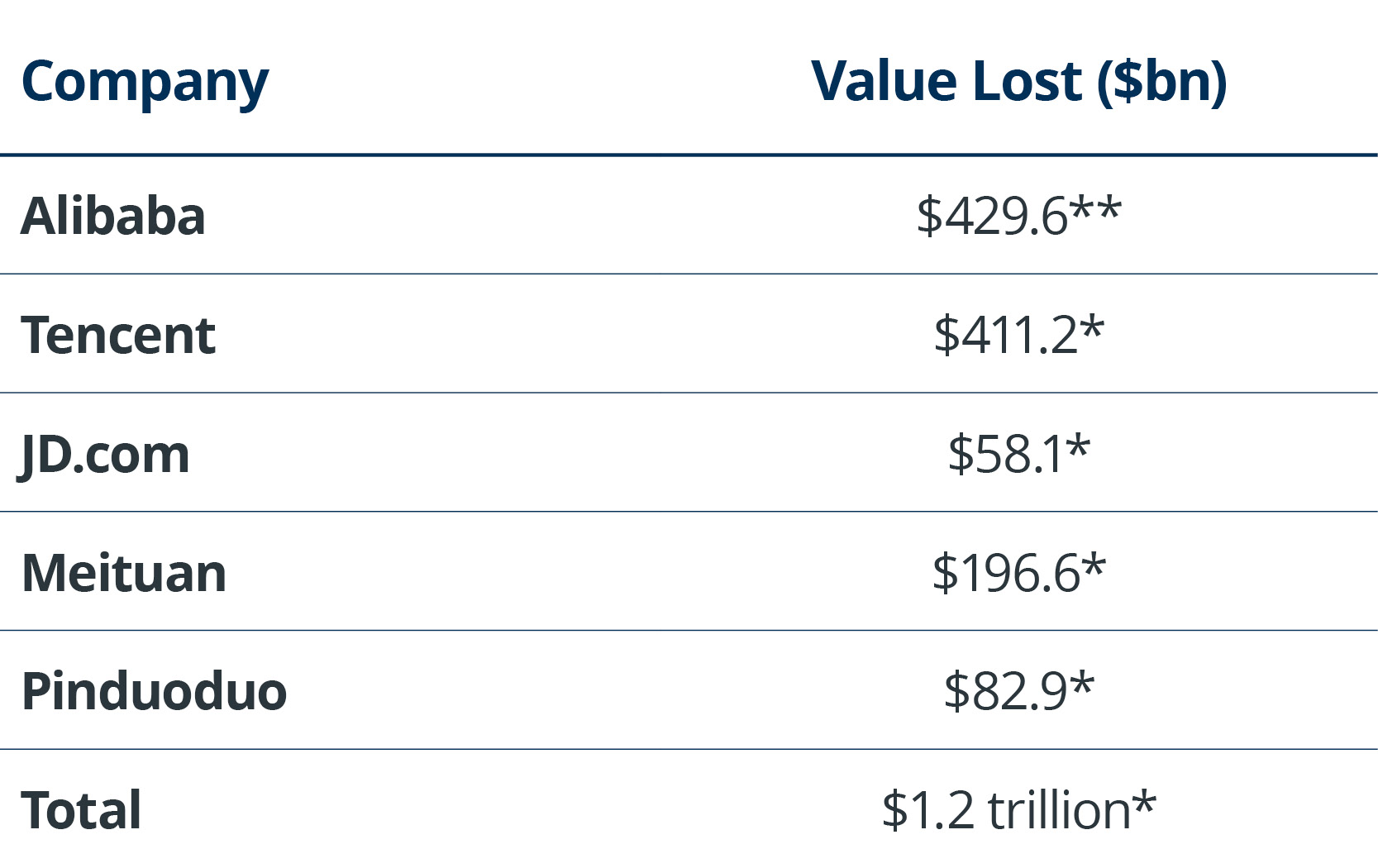

Take AliBaba, as it was the first to come under the scrutiny of China’s State Administration for Market Regulation (SAMR).

On April 10, 2021, regulators handed AliBaba the biggest fine in corporate history. A record $2.8 billion for abusing its dominant market position (in context: c.10% of their free cash flow and only 4% of its cash on hand for the company), calling on other tech giants to conduct “comprehensive self-inspections” to ensure they are adhering to competition law.

After all this focus and negative sentiment, AliBaba’s forward P/E sits at just 17.

Cheaper than Unilever. AliBaba is also sitting on an astounding $78 billion in cash with an impressive $250 billion in assets.* In addition, its P/S is cheaper than that of the NASDAQ Index, by a third. You get the point.

A relatively cheap stock, with the following current core business performance:

Core E-commerce +35%*1

Cloud Computing +29%*

International E-Commerce +54%*

Some investors will swoop in and see these events as a massive buying opportunity, but we believe they should proceed carefully (or at least with a long-term time horizon).

It is difficult to evaluate the material effects of government regulations on valuations.

When government policy is stable this doesn’t present too much of an issue, but now we’re seeing valuations reflecting investor fear that the Chinese government will put the brakes on future growth. As markets react, we believe there are opportunities for investors to be found amongst the volatility.

Some further food for thought, China’s crackdown may not be confined to purely Chinese securities. China has shown its insatiable appetite for luxury goods, and according to CNBC, 45% of global luxury sales come from China. More specifically, CNBC also highlighted that LVMH gets 1/3 of its global sales just from China (H1 2021). Also, LVMH (as at the time of writing) is the fourth largest holding in the MSCI Europe Index.

If you’re targeting a more diversified approach to gaining exposure to these names, thematic investing can help lead to a broader, more inclusive portfolio. However, if you think there’s more to come from China’s regulators, it might be best to sit this one out for now.

1Source: Factset

Important Information

This financial promotion is issued by First Trust Global Portfolios Management Limited (“FTGPM”) of Fitzwilliam Hall, Fitzwilliam Place, Dublin 2, D02 T292. FTGPM is authorised and regulated by the Central Bank of Ireland (“CBI”) (C185737). The Fund is also regulated by the CBI.

Nothing contained herein constitutes investment, legal, tax or other advice and it is not to be solely relied on in making an investment or other decision, nor does the document implicitly or explicitly recommend or suggest an investment strategy, reach conclusions in relation to an investment strategy for the reader, or provide any opinions as to the present or future value or price of any fund. It is not an invitation, offer, or solicitation to engage in any investment activity, including making an investment in a Fund, nor does the information, recommendations or opinions expressed herein constitute an offer for sale of a Fund.

Share