“The case for digital transformation has never been more urgent or clearer. Digital technology is a deflationary force in an inflationary economy.”

Satya Nadella

Key takeaways

- The CHIPS Act promises to inject $52.7 billion to stimulate a return to U.S. manufacturing of semiconductors - away from Asia.

- With the U.S locked in a race with China, restrictions have been tightened, essentially banning any chips created in the last 10 years.

- Geopolitical tensions have escalated over control of Taiwan – perhaps the most strategically important country in the entire microchip value chain.

- How does this impact Thematic Investors?

Much like how oil fuelled the rise of industrial economies in the last century, the semiconductor industry has become arguably as important, expected to power the next decade of growth. Technologies like the IoT and clean energy, and innovations like blockchain and cloud computing are almost entirely reliant on semiconductors. When, in 2021, the world witnessed both the insatiable demand and severity of the global chip shortage affecting automotive behemoths like Toyota and Ford, smartphone manufacturers Apple, and electronics companies like Sony, the world grasped the importance of semiconductors.

So, have chips become the new oil?

The Geopolitics of Chips

Semiconductors have increasingly become a political and geopolitical football. Like oil, the microchip industry has become a key resource for countries. With the U.S. locked in a race for technological superiority and influence with China, the global battle for semiconductors raises the issue of strategic risk. While China currently lags the U.S. in terms of possessing cutting-edge manufacturing, it was under Trump’s tenure that the U.S. government first sought to restrict China’s access to critical manufacturing tech. Now, the U.S. has gone a step further, expanding its restrictions, cutting off the most sophisticated chips typically used for AI or the latest smartphone, or more importantly, military applications. In the world of chip manufacturers, smaller is better; the smaller nanometer (or “nm”) the more advanced the chip, thus the U.S. raising the thresholds on restrictions to 14nm (from 10nm) encompasses a broader range of semiconductors 1. In iPhone parlance, these restrictions would have banned any chips created in the last decade (since the iPhone 4S back in 2011).

These latest restrictions come hot on the heels of recent warnings by China’s President Xi Jinping suggesting he is willing to use force to reassert control over Taiwan. Taiwan Semiconductor Manufacturing Company (TSMC) has become vitally and strategically important to the microchip value chain, producing almost two thirds of the world’s chips 2. This situation has forced policymakers to consider the implications of its military being cut off from these chips, precipitating the CHIPS Act.

• increasing U.S. competitiveness

• reducing America’s over-reliance on foreign-made semiconductors

America’s declining chip production (its share of global production has declined over the past 30 years, from 40% to just 12% today3), together with the recent heightened geopolitical tensions, catalysed the new bipartisan agreement. While the U.S. boasts 12 of the world’s top 15 semiconductor companies4, it severely lacks “fabs” (advanced fabrication plants), which ultimately control chip production. The CHIPS Act specifically addresses America’s lack of autonomy in the microchip value chain, given its over-reliance on inputs from contract manufacturers, like Apple being TSMC's largest client5.

With government funding now secured, numerous fabs in places like Texas, Arizona and Ohio are planned over the next few years, taking production back to the States. But this isn’t the only incentive for U.S.-based manufacturers. New York committed $10bn6 in corporate tax breaks for chip makers who build or expand semiconductor fabrication plants, within the state. Many more states are expected to follow suit.

Powering Your Portfolio?

Megatrends powered by long-term growth in technology and innovation will require semiconductors to function (and grow). Currently, global demand for chips is rising at an incredible rate and will likely only accelerate as devices become smarter and increasingly connected. We see a significant opportunity for some companies at the heart of the digital and clean energy transformations, across the entire value chain.

Who Benefits?

Aside from the chip makers themselves, both Clean Energy and Smart Grid companies potentially stand to benefit. Tailwinds include an increased supply of semiconductors, cheaper costs to acquire them domestically, and less chance of supply chain disruptions. The automobile industry, particularly EVs, would also benefit. In 2021, a new vehicle contained close to 300 different semiconductors, a massive 40% increase from just two years earlier7. Meanwhile, Ford’s new EV for example, is estimated to use 3,000 chips.7

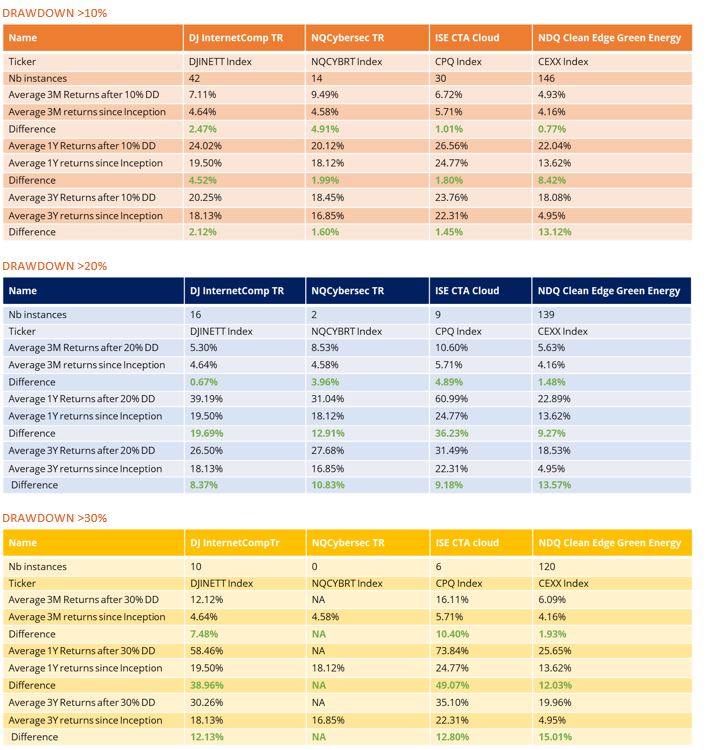

Below we've highlighted some thematic indices and their respective exposure to semiconductors:

Data as at 31 August 2022.

Since publishing this article (14th September) Apple revealed it would be using TSMC’s 3 nm chip in its new iPhone 14, making larger microchips obsolete and further inhibiting China’s powers8.

Sources

1. Electronic360.com

2. Voanews.com

3. Semiconductors.org (2021)

4. Companiesmarketcap.com (August 2022)

5. Statista, 2021

6. Syracuse.com (June 2022)

7. CNBC (September 2021)

8. Appleinsider.com (August 2022)

Important Information

References to specific companies should not be construed as a recommendation to buy or sell shares or other financial instruments issued by those companies, and neither should they be assumed profitable. You should consider the fund’s investment objectives, risks, and charges and expenses carefully before investing.

This marketing communication is issued by First Trust Global Portfolios Limited (“FTGP”) of 8 Angel Court, London, EC2R 7HJ. FTGP is authorised and regulated by the UK Financial Conduct Authority (register no. 583261).

Nothing contained herein constitutes investment, legal, tax or other advice and it is not to be solely relied on in making an investment or other decision, nor does the document implicitly or explicitly recommend or suggest an investment strategy, reach conclusions in relation to an investment strategy for the reader, or provide any opinions as to the present or future value or price of any fund.

Share