So far since the start of the year, we’ve seen new Coronavirus variants, continued supply chain pressures, higher inflation, Fed tightening, energy price spikes, and the Russian invasion of Ukraine.

For investors, trying to forecast to Friday is challenging enough, let alone trying to project further into the future. With rising inflation, interest rates and near-term volatility impacting market sentiment, where can investors look for as much certainty as possible?

The more convincing and predictable the revenue stream in the present moment, the more confidence investors can have in returns over time.

Where can investors find forced revenues?

Last quarter, we looked at the how the massive increase in digital presence for companies and consumers alike, cloud computing and by extension cybersecurity, have become a necessary investment for businesses.

Effectively they have become ‘digital utilities’ meaning even in an inflationary environment or an economic downturn, companies will still need to invest in these areas.

Much like the defensive play traditional utilities used to be, companies at the forefront of the cloud computing and cybersecurity industries are providing highly scalable essential services, with high switching costs for consumers.

A large number of players in the space also run subscription models which also provide more visibility and potentially more predictable, stable revenue streams.

In periods of volatility, another area of forced revenue that investors may benefit from targeted exposure is to companies at the intersection of thematic investing and real estate.

Combining both the innovation and growth of disruptive industries in which companies are essentially being forced to invest in or risk being left behind, alongside the predictable revenue of real estate.

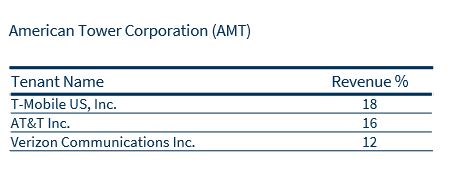

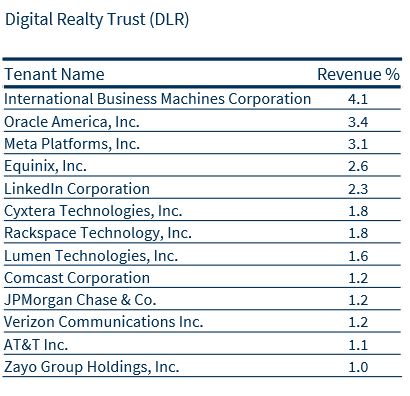

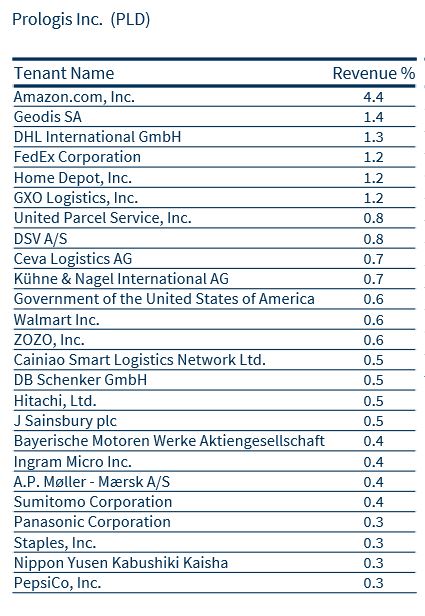

REITs have recurring revenue models by default, as the product is essential to tenant function, can’t be used without the tenants paying for the service, the cost of switching is high, and as the service is location-based, there tends to be low competition. Add to the mix, that global demand for connectivity is driving the need for meaningful, consistent investment in the digital and physical infrastructure underpinning this.

Share