“The case for digital transformation has never been more urgent or clearer. Digital technology is a deflationary force in an inflationary economy.”

Satya Nadella

Key takeaways

- Investors are becoming increasingly concerned about the health of the real estate sector in general, and commercial real estate in particular.

- Real estate should always be included in a diversified portfolio, but investors should reconsider their true exposure.

- We provide a thematic lens to investors' commercial real estate concerns, focusing on two areas with positive tailwinds: data centres and e-commerce warehousing.

- The Alerian Disruptive Technology Real Estate Index offers targeted exposure to the physical infrastructure that is powering the digital revolution.

Addressing the problem

In May, Charlie Munger, Berkshire Hathaway’s vice-chair warned of a developing storm in the U.S. commercial real estate (CRE) market. Mr Munger commented that “we have a lot of troubled office buildings, a lot of troubled shopping centres, a lot of troubled other properties. There’s a lot of agony out there.” Apollo Global Management went one step further, suggesting the sector was flashing a warning signal to investors, and was likely the “next shoe to drop”.

The last 18 months have seen commercial real estate values hurting owing to a combination of rising rates, moderating growth and tightening credit markets. This pain has intensified following the failures of Silicon Valley Bank, First Republic and Signature Bank which then raised concerns about other regional banks that account for the bulk of commercial real estate loans.

Office-based REITs dropped 37.6% in 20221 and another 12% so far in 20232, its lowest reading since mid-2009. For America’s largest office market, New York City, a recent study predicted that by 2029 the market's value will remain an astonishing 43.9% below pre-pandemic levels3. Offices are clearly weighing on the broader REIT index, but that doesn’t mean that investors should shun REITs altogether.

Evidently there has been a clear reaction to a post-pandemic world (together with the rapid pace of digitalisation), for how businesses reacted, impacting all industries including real estate; where some faltered and failed, including malls and office space and some were able to adapt and flourish.

Fundamentally real estate’s value is derived from how it is used.

Real estate exposure in your portfolio

Real estate has long been a key building block of investor portfolios, offering broad diversification, an inflation hedge and of course meaningful long-term return potential. REITs are required to pay out 90% of taxable income as dividends to shareholders, giving investors access to one of the most consistent streams of cash; tenants paying their rent.

When investors think real estate they often think of residential, offices, or shopping malls and perhaps a little less about the physical structures that enable modern technology, such as tenants renting server space and e-commerce vendors renting warehouses.

In our opinion, REITs deserve a place in an investor's portfolio because of their positive attributes. However, given the concerns we highlighted above, we could hardly blame real estate investors for having allocation worries. However, what alternatives does a real estate investor have?

Here’s where a thematic lens can potentially help.

Scalpel vs hammer: using Thematics for a more precise allocation

Digitalisation, from themes like cloud computing, artificial intelligence (“AI”), and e-commerce are driving a new world order when it comes to real estate. The physical infrastructure underpinning these technologies, such as data centres and e-commerce warehousing have become the in-demand “landlords” of our digital economy, in our opinion. Society relies on digital applications, and the data creation, storage, and processing they require, for pretty much every aspect of our modern lives, especially AI. Let’s look at some of the tailwinds for these themes.

Tailwinds for datacentres

With forecasts of almost four times more data being produced and consumed in 2023 than 20184 it’s hardly surprising that demand for data centre capacity is at an all-time high, even after rising by 137% in 20225. This, combined with the unique supply dynamics of semiconductors, are forcing global enterprises to become tenants of datacentres. Further, according to renowned investors Andreessen & Horowitz, demand for computing power is outstripping supply by 10x6.

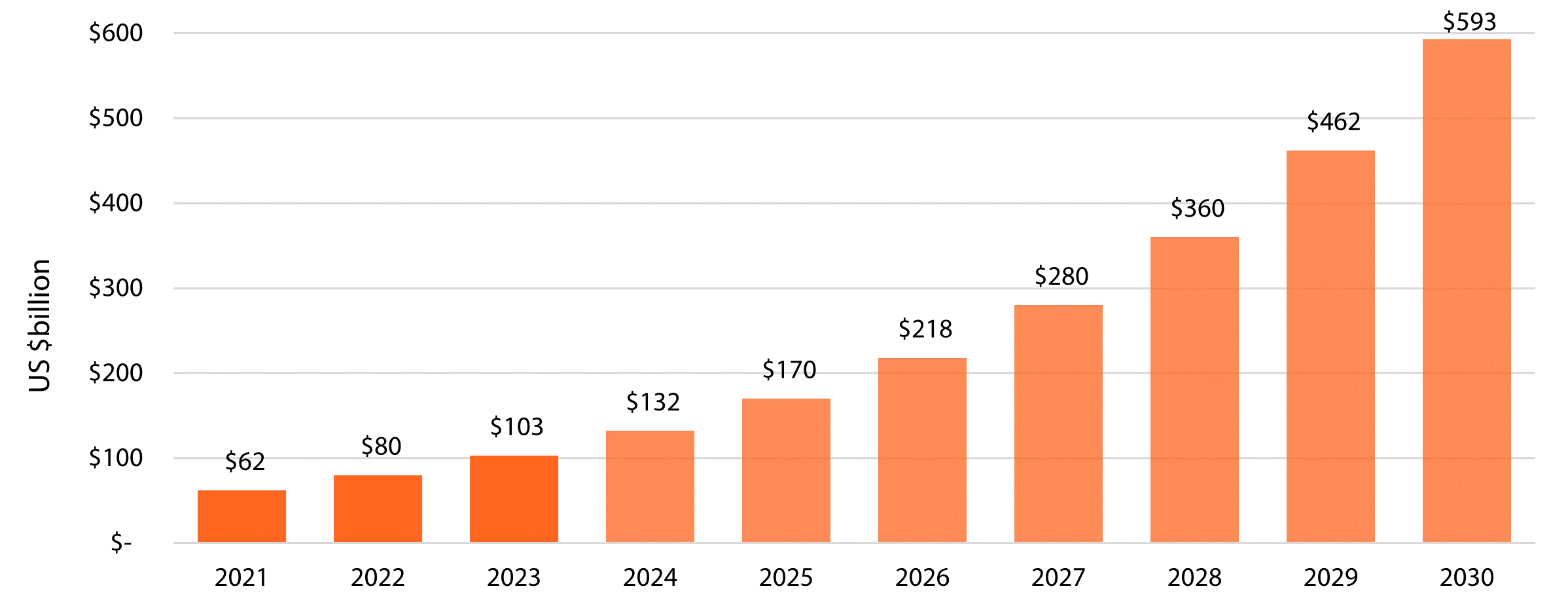

Thought exercise: what would you do, as an AI start-up or a large company, if you couldn't get your hands on an Nvidia H100 processor or, better yet, the DGX H100 (their entire AI Platform)? You would probably rent it from Equinix or one of the 20 DGX-ready datacentres run by Digital Realty that are located all over the world. The fact that the market for data centres is expected to grow five times by the end of the decade should come as no surprise (see chart below)7.

Let’s think like a real estate investor. Data centre vacancy rates at the end of FY22 stood at record lows of 3.2%8, conversely NYC office vacancy rates are at c.22.7%9. Supported by the booming demand for AI-focused data centre chips and by strong earnings results from these REITs, data centres are showcasing their impressive pricing power.

Hyperscale data centre market size (2021-2030)

Source: www.precedenceresearch.com

It’s worth remembering that as a REIT, both Digital Reality and Equinix must pay out 90% of these cashflows to you. The former has a strong track record of returning value to its shareholders in the form of dividend payments (equivalent to a 4.1% yield)10, while paying and increasing their dividends in each year in the past 18 years.

Tailwinds for e-commerce warehousing

We remain equally optimistic about the outlook for the industrial REIT theme, which comprise the warehouses of e-commerce companies, like Prologis, labelled as “Amazon.com’s landlord”. Today, Prologis is the largest REIT in the world11.

Going forward, demand for logistics space is expected to grow by a CAGR of 11.8% until 203012. We believe that this growth will be driven primarily by two main factors; a combination of increasing e-commerce penetration as a percentage of sales and higher inventories in proportion to sales as retailers target larger inventory buffers post-Covid.

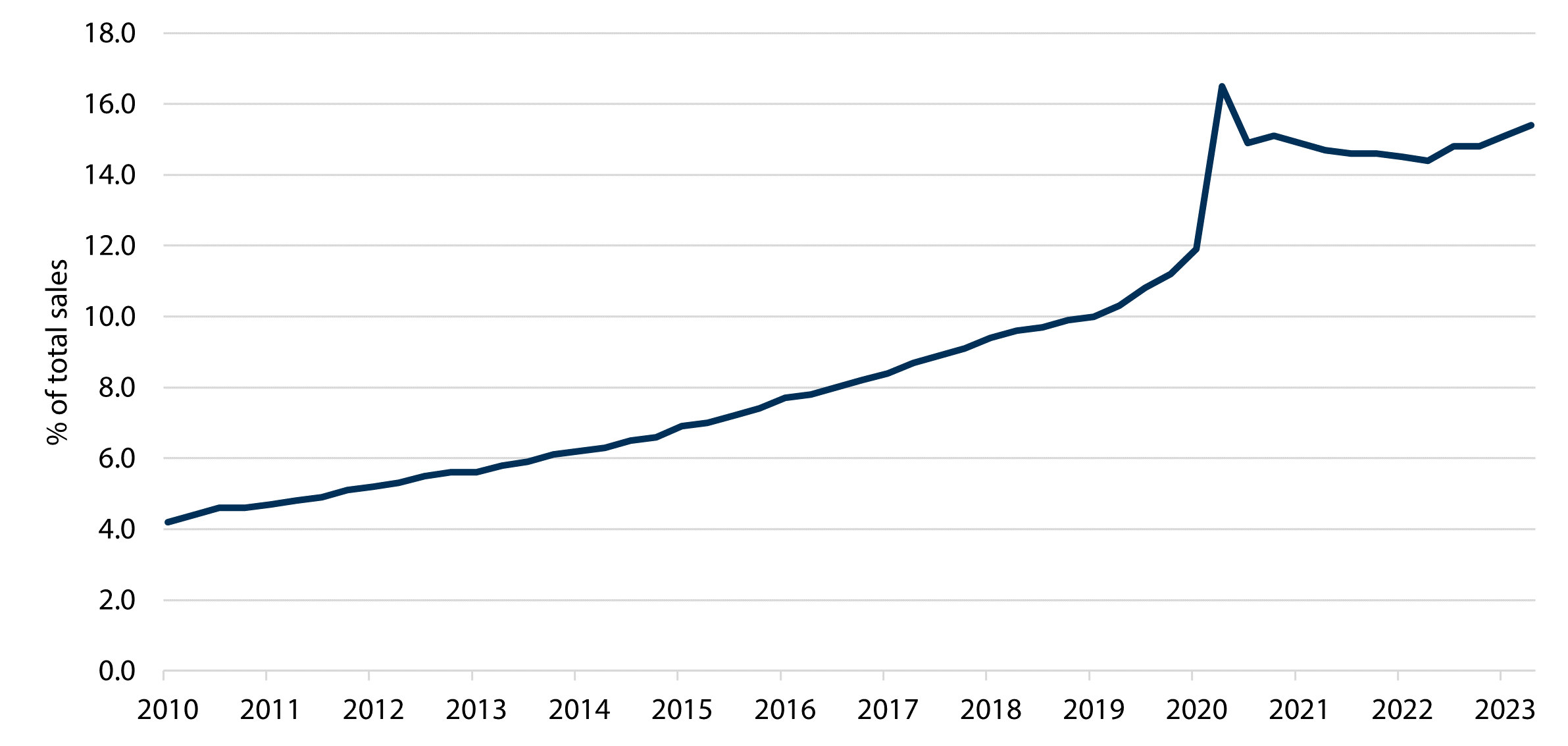

While expected to reach a staggering 26% of all U.S. retail sales by 202513, surprisingly, e-commerce accounts for only 15.4%* today (see chart below). U.S. e-commerce sales are forecast to grow from $0.9 to $1.4 trillion over the next three years14, and meeting this demand will require an addition of millions of square feet of warehouse and distribution space. It’s likely that a significant amount of new construction (as well as the repurposing of existing structures) will be needed in the next few years just to match our current demands.

U.S. e-commerce retail sales as a % of total sales

Source: Federal Bank of St. Louis. Q1 2010 - Q2 2023

Purely from a real estate perspective it’s worth appreciating that for every $1 billion growth in e-commerce sales, 1.25 million sq ft of new distribution space is required to support that because e-commerce requires three times as much space as brick and mortar stores15. For investors, this seems like a good opportunity for those companies which own this space, real estate companies like Prologis, whose vacancy rate sits at just 2.5%16.

Using Thematic ETFs for real estate exposure

The Alerian Disruptive Technology Real Estate Index (“LANDX”) provides targeted exposure to those companies which provide the physical infrastructure which is powering the digital revolution from e-commerce warehousing and logistics, data centres and cell towers and nothing else. No exposure to malls or offices.

While LANDX did suffer from contagion from last year’s broad bear market, down 25.91% in line with the MSCI World REIT index, year-to-date it has move ahead of the pack, up 7.10% vs 3.73% driven by both its data centre and e-commerce warehousing exposure17.

LANDX is currently 30% off its all-time high, but with an index yield of 3.49% and a price-to-book ratio of just 2.0417, investors may find that these fundamentals offer an attractive entry point to participate in the physical investment in the digital economy.

Share