Common belief among investors is that Europe is the land Growth forgot. Equities in the region are usually held for their solid, stable performance, but rarely generate the buzz which some of the more “dynamic” names in the US and Emerging Markets enjoy. There’s just this perception that there are no dynamic disrupters in Europe. Are these beliefs backed by data? Surprise! Not really.

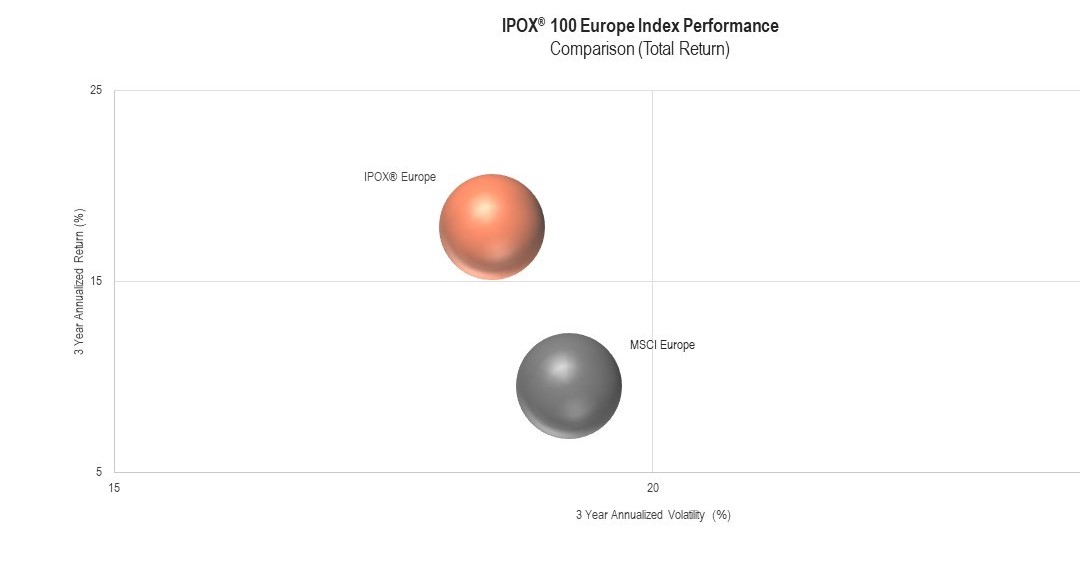

Here’s a data point to set the scene: In 2020 the MSCI Europe Index delivered a return of -3.32%.

Just as you’d expect; limited growth was further dampened by a slow and painful recovery from March’s Covid drop.

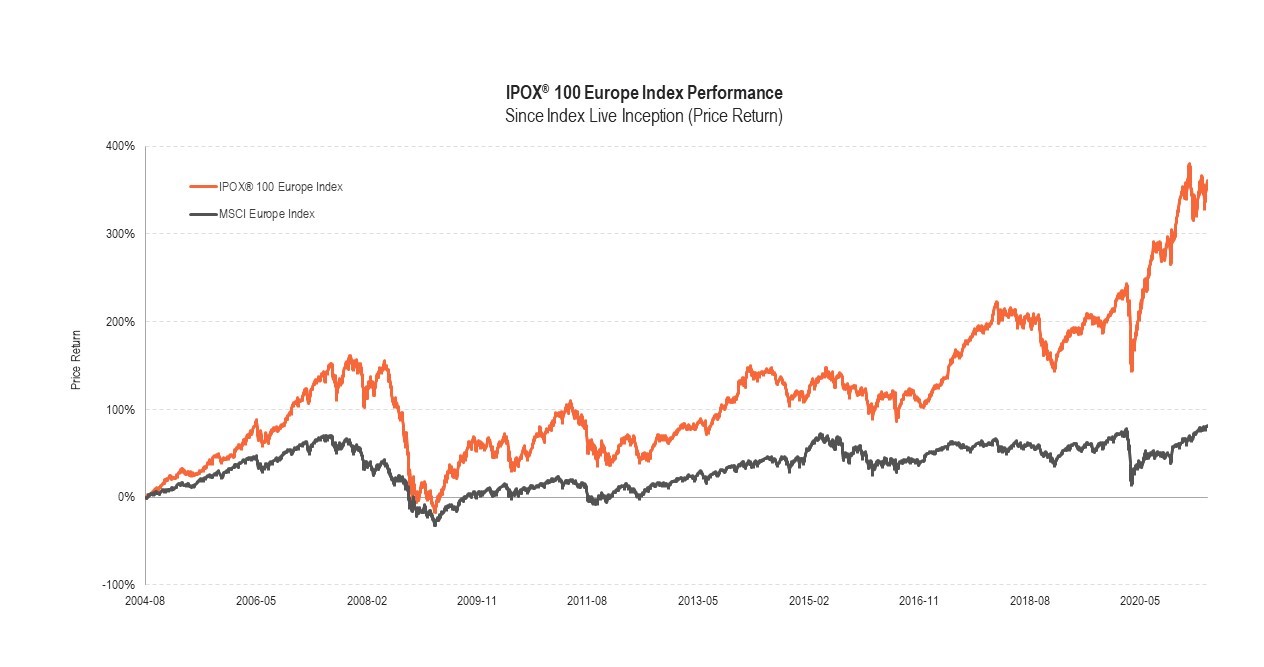

Meanwhile, the IPOX Europe Equity Index, which holds the 100 largest European IPOs and Spin-Offs for roughly a four-year period, delivered a 24.13% return for the year*.

With that in mind, let’s talk European IPOs.

Key takeaways

- The IPOX Europe Equity Index, which holds the 100 largest European IPOs and Spin-Offs, delivered a ~20% higher return than the MSCI Europe Index in 2020

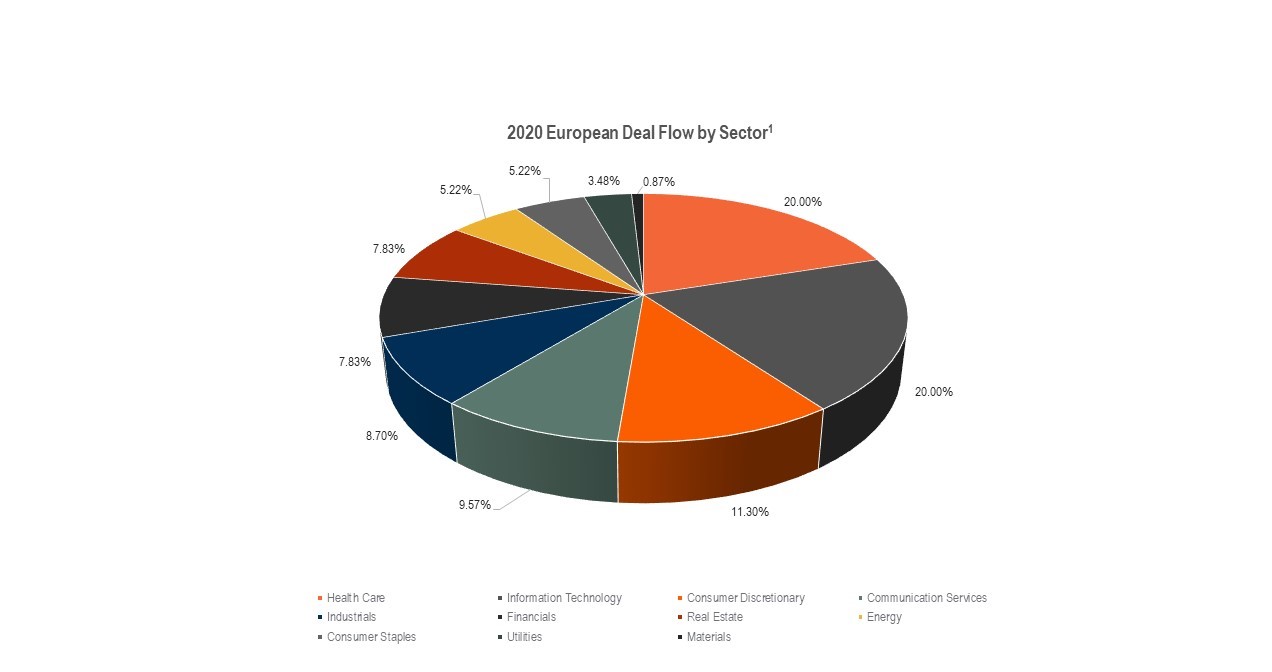

- IPOs are not just healthcare and technology names - in Europe 60% of IPOs are not in these sectors

- European IPOs and spin-offs represent a highly attractive theme, backed by a wealth of data and a strong track record

*Source: IPOX® 100 Europe Index as of 30/04/2008 to 30/04/2021. IPOX Schuster LLC. IPOX® 100 Europe Index (IPOE Index) was launched on December 30, 2005, data prior to the launch date is back-tested data. Past performance is no indication or guarantee of future performance. Past performance is not a guarantee of future results and current performance may be higher or lower than performance quoted. Investment returns and principal value may fluctuate and shares when sold or redeemed, may be worth more or less than their original cost. Performance shown in EUR. The return on your investment may increase or decrease as a result of currency fluctuations if your investment is made in a currency other than that used in the past performance calculation.

IPOs and Spin-offs as a source of alpha

New Listings are often drivers of economic growth and innovation. IPOs and spin offs - regardless of where a listing takes place – have a unique returns dynamic.

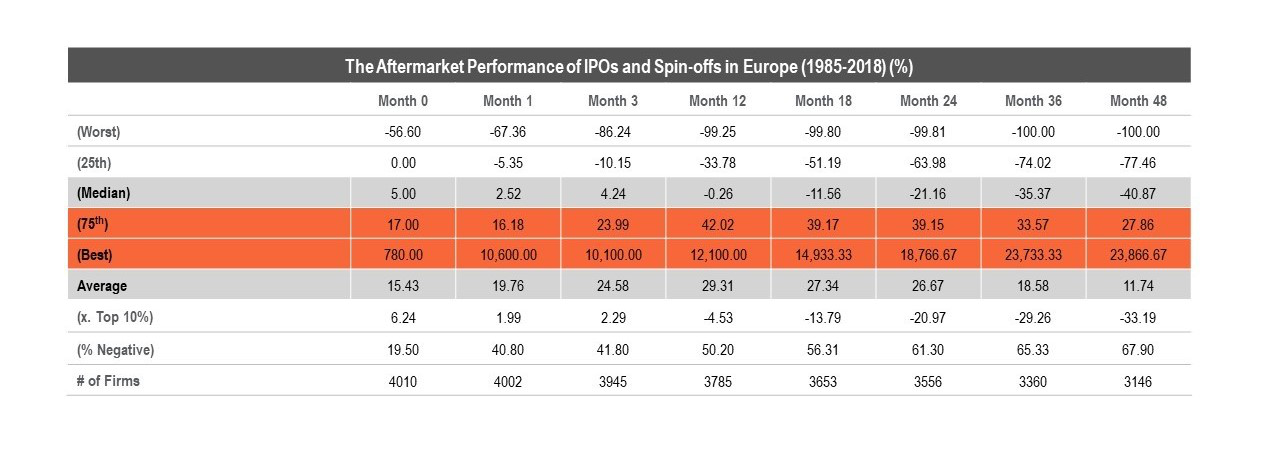

For example, average first day returns have historically been significantly positive, providing compensation to both pre-IPO investors and syndicate participants. This is commonly known as the practice of “Underpricing.”

Later, “true” a valuation becomes clearer when new listings build an earnings record. Thus, within the first years of an IPO, the returns distribution diverges: while many IPOs perform poorly, many deals significantly outperform the market, with the winners more than making up for the losers.

Myth-breaking: How IPO trends manifest in Europe

In Europe, the top quartile of IPOs and Spin-offs from 1985-2018 returned nearly 34% after three years. Very different from the typical perception of slow-growing companies! This is out of a sample of 3,360 firms!

Share