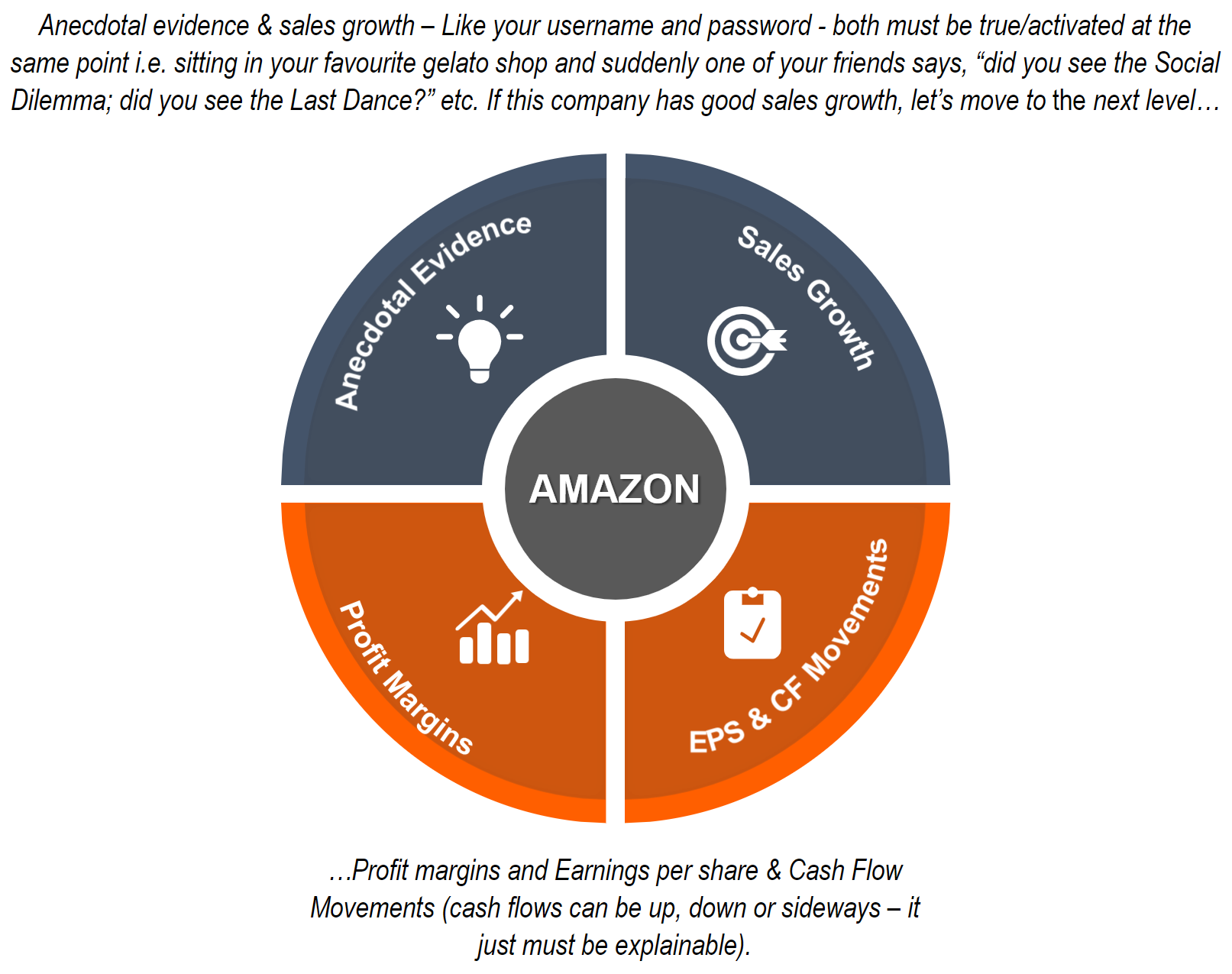

Evaluating rapid growth stocks (The Four Quadrant Matrix)

Let’s be clear, just because we believe we are not in a bubble DOES NOT mean an investor can’t lose on their investment and investing in rapid growth businesses can be a bumpy ride. See any strong returning stock ever. So, how do you evaluate stocks that are growing at a rapid pace? Here is our 4 quadrant matrix to evaluate rapid growth businesses.

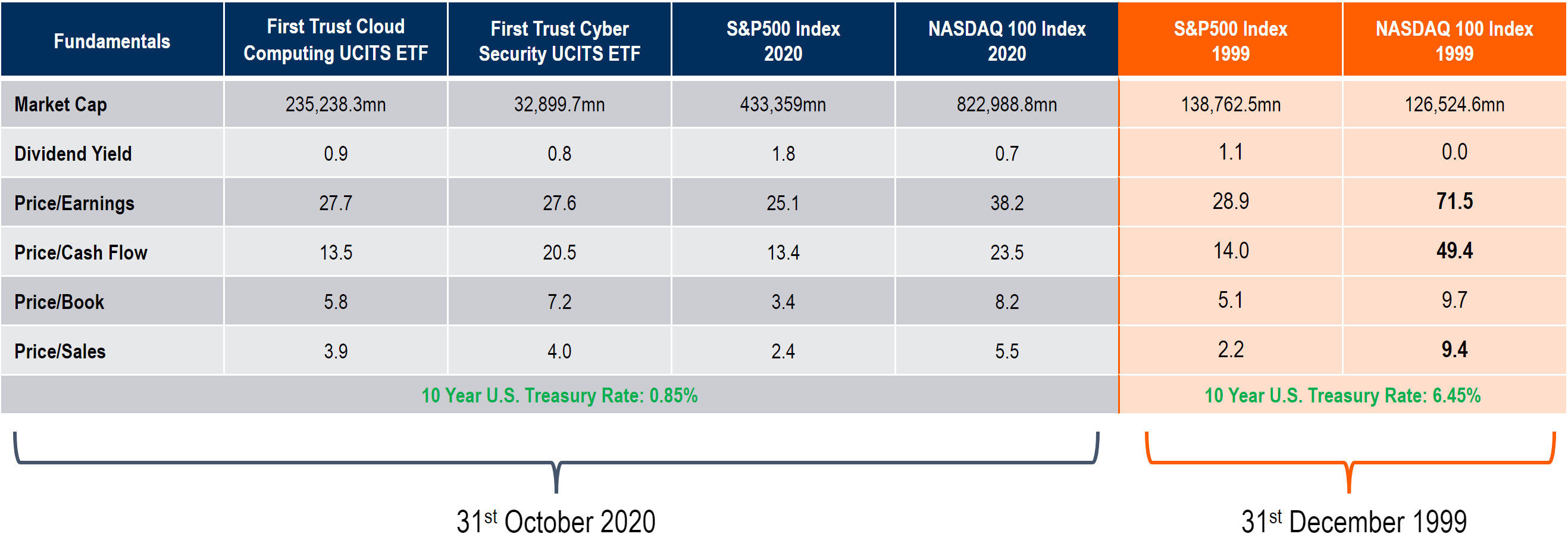

But What about PE? The Failings in Using PE Here

We think that price to earnings is not a good valuation metric for rapid growth businesses, but that doesn’t mean you can’t use traditional fundamentals such as p/s, which we feel is more than effective. However, don’t forget the other two dimensions of price to sales; sales growth and margins. Example: two companies grow revenues of £100 by 10%, and one has 10% margins and the other 50%. One company generates £5 while the other only £1 from the “same growth.” Add a year and you can see how this can start to compound on itself.

Basket Case: Amazon

Over the last 5 years, if you used P/E as your fundamental base, you’d never have bought into Amazon. Clearly it was a good investment, so what else could we have used?

If we look at 2015 as the foundational moment for this company, EPS went from negative to positive (by the way, this may also be happening to Tesla this year). The 5yr average price return was 47.2% and it did this on just 26% sales growth. This was because on a cashflow basis, Amazon produced 62% cumulative annual growth on the above sales number. How? Because their margins moved from 29 to 41%. Why? Largely, because of just three letters: AWS**.

One more example of how even the most professional among us can be wrong. Amazon is in the top 3 or 4 most heavily covered stocks on the planet. The consensus analyst estimates forecast that Amazon would have $1.86 earnings per share in Q2. They were wrong, dead wrong. They earned $10 a share! Interestingly instead of an 18.76 EPS for the year, they are now forecasting 30 EPS. EARNINGS!….for Amazon. 5+ years ago, this was a joke.

We've heard that all before says the experienced vet, “That’s what they said in ‘99.” Well, here are the P/S ratio and weighted sales growth numbers for our thematic ETFs and benchmarks.

Share